NOTE: Some refactoring work for SettlementPeriods are being considered for the next draft.

16.1 Introduction

This section provides a detailed description of the product architecture for commodity derivatives. FpML provides support for commodity swaps (whether fixed-float and float-float, or weather/weather), traditional commodity options (American, European and Asian) and its variations, as well as Basket and Digital options . FpML also supports contracts written on physically-settled electricity, natural gas, oil, coal, and environmental commodities. FpML provides support for physically-settled precious and non-precious metal forwards. At the core of the architecture is a representation for a commodity underlyer which is used within the commodity products, as well as, other products such as equity baskets. A representation of gold interest rate swap (official name: Gold Forward Offered Rate) has also been introduced, which is used within the commodity products but that can also be used within other products such as IRS.

For an overview of the commodities coverage in FpML and its linking with the legal documentation see the following document: FpML Commodities Coverage Matrix (pdf file)

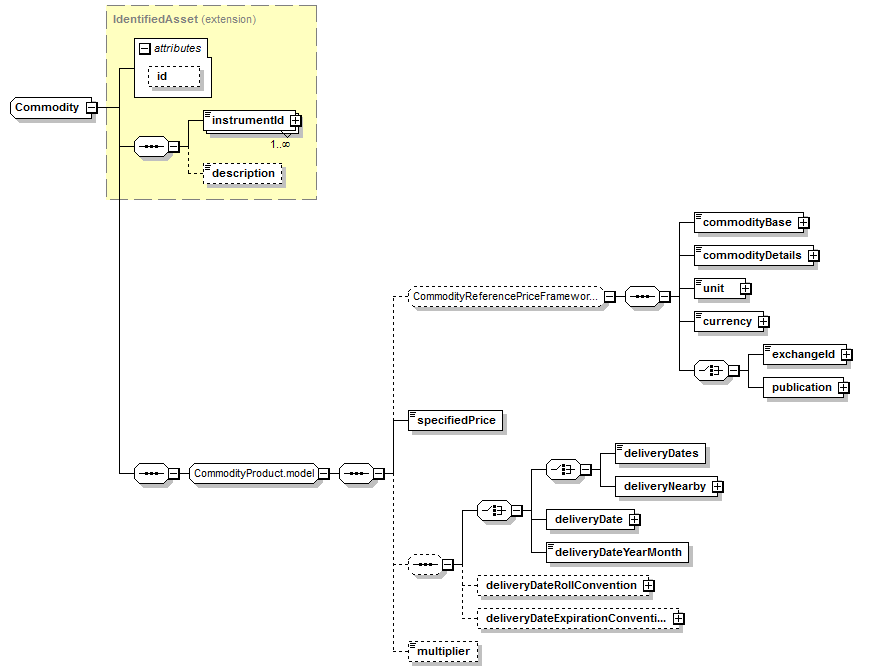

The 'commodity' underlyer identifies the market price on which the OTC contract is written. The structure of the 'commodity' underyer follows the ISDA Commodity Reference Price Framework. FpML defines a number of global elements in the FpML schema for various types of assets The 'commodity' underlyer follows the same model.

|

|

|

The 'instrumentId' and the 'description' elements are derived from the IdentifiedAsset type, which is used by multiple underlyers. The 'instrumentId' contains the unique identifier for the asset, and is intended to hold a Commodity Reference Price in the format set out by ISDA in the 1993 or 2005 Commodity Definitions. However, a CUSIP, ISIN, or any other identifier could also be used. The 'description' contains the name of the asset.

The following sequence of elements is optional and they are specified only in the event that no ISDA Commodity Reference Price or other standard identifier for a commodity 'index' exists.

|

|

|

specifiedPrice-The 'specified Price' describes the nature of the underlying price that is observed. It must be be stated in the underlyer definition as it is not defined in the Commodity Reference Price. Example values of 'specifiedPrice' are 'Settlement' (for a futures contract) and 'WeightedAverage' (for some published prices and indices).

deliveryDates-No Annotation Available

deliveryDateRollConvention-The 'deliveryDateRollConvention' specifies, for a Commodity Transaction that references a listed future via the 'deliveryDates' element, the day on which the specified future will roll to the next nearby month prior to the expiration of the referenced future. If the future will not roll at all - i.e. the price will be taken from the expiring contract, 0 should be specified here. If the future will roll to the next nearby on the last trading day - i.e. the price will be taken from the next nearby on the last trading day, then 1 should be specified and so on.

multiplier-The 'multiplier' specifies the multiplier associated with the Transaction. The 'multiplier' element has two uses: (1) for Freight Transactions or any Calculation Period specified for a Freight Transaction, if an amount is specified as the Multiplier then it is captured by this element and (2) if the Transaction is a heat rate option, the heat rate multiplier is represented in this element. If multiplier is not provided, multiplier is assumed to be 1. (i.e. rate source states 1 BBL of Oil as 90 Dollars. Multiplier of 10 will change the value to 900 dollars.)

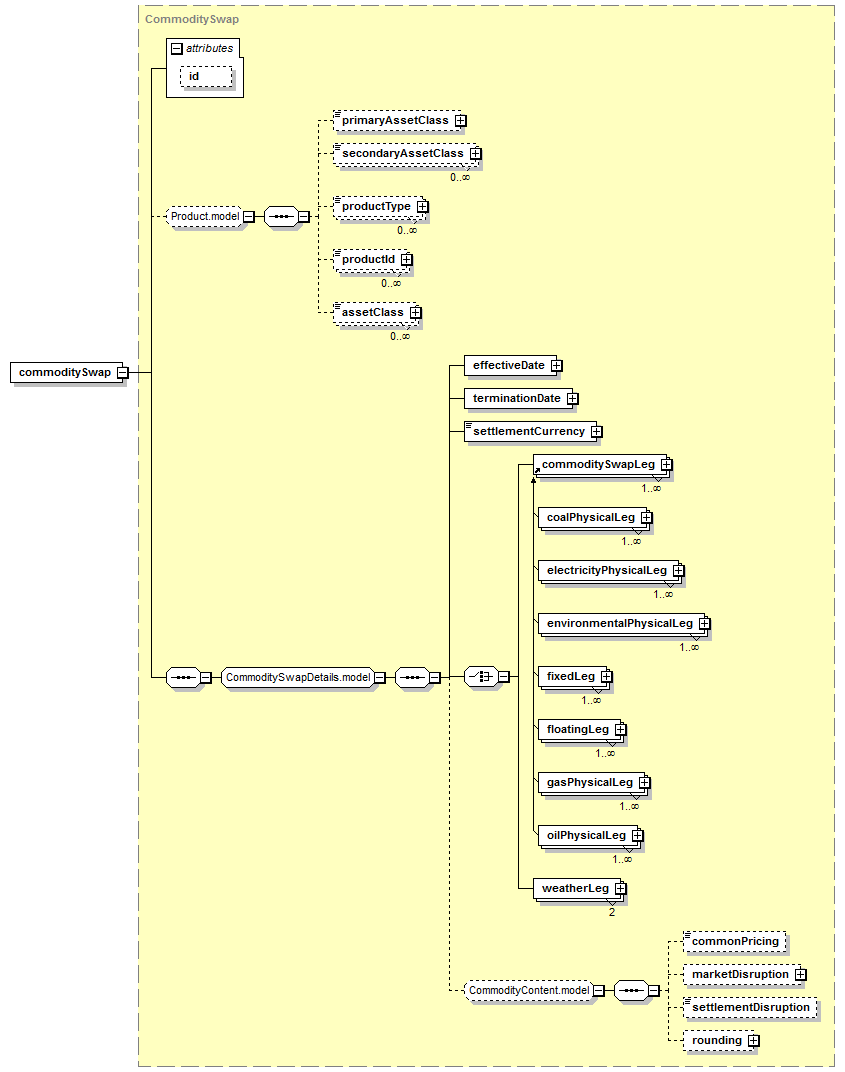

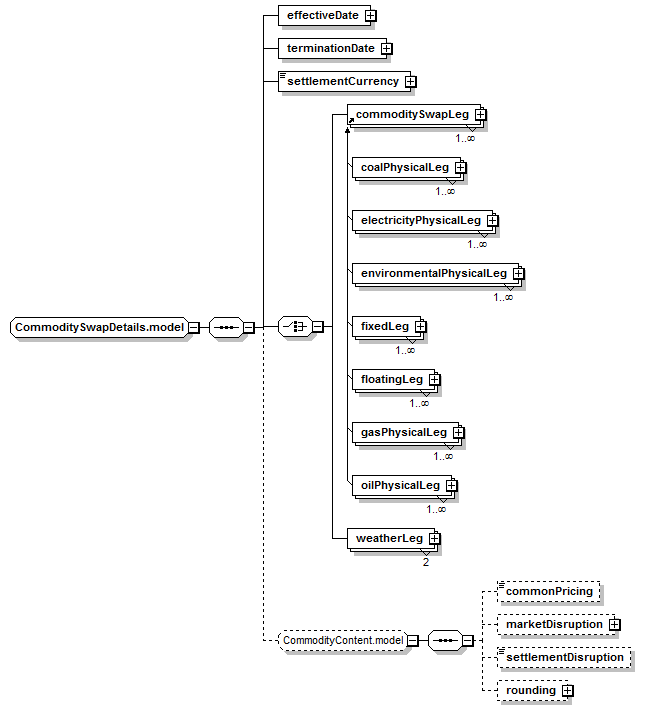

CommoditySwap-The commodity swap product model is designed to support fixed-float swaps, float-float swaps, fixed vs. physical swaps, float vs. physical swaps as well as, weather specific swaps. Its design is fully compatible with other FpML products and the product reuses standard common types.

As with all products in FpML, commodity swaps are accessed through a global element, 'commoditySwap', which substitutes for the 'product' element used in trade structures. The following diagram outlines the product structure.

|

|

|

The 'commoditySwap' structure defines parameters for product-related information (e.g. dates, rates, underlying commodity, price source, etc.). Other trade-related information (e.g. trade date, identifiers, legal documentation, etc.) is held in the containing 'trade' structure.

The 'commoditySwapLeg' element is placeholder within commoditySwap structure for the actual commoditySwap swap legs (e.g. 'fixedLeg' and 'floatingLeg'). The 'weatherLeg' is modeled as a choice to 'commoditySwapLeg' because weather index transactions are strictly financially-settled transaction and always structured with two legs, each of which is a 'weatherLeg'.

The repeating 'fixedLeg', 'floatingLeg', 'weatherLeg' elements contain the details of any scheduled cash payments or exchanges during the life of the instrument and are described later. A simple commodity swap will contain two legs, typically one fixed and one floating, but the repetition allows more complex multi-legged structures to be represented.

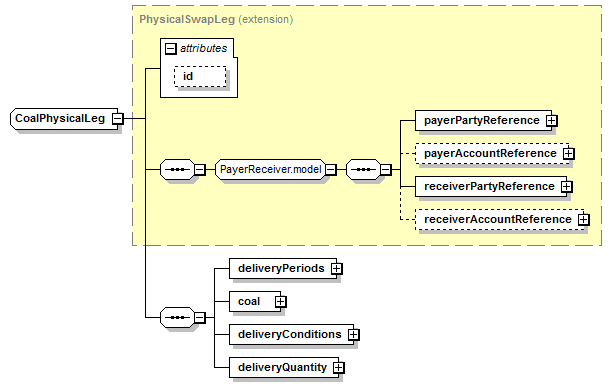

Physical settlement of swaps is represented using 'coalPhysicalLeg', 'electricityPhysicalLeg', 'gasPhysicalLeg', 'oilPhysicalLeg', 'environmentalPhysicalLeg' paired with 'fixedLeg' or 'floatingLeg' - see details in the Physical Leg section.

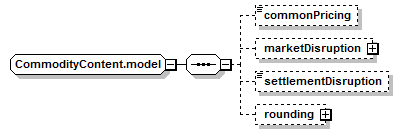

CommodityContent.model-Items common to all Commodity Transactions.

|

|

|

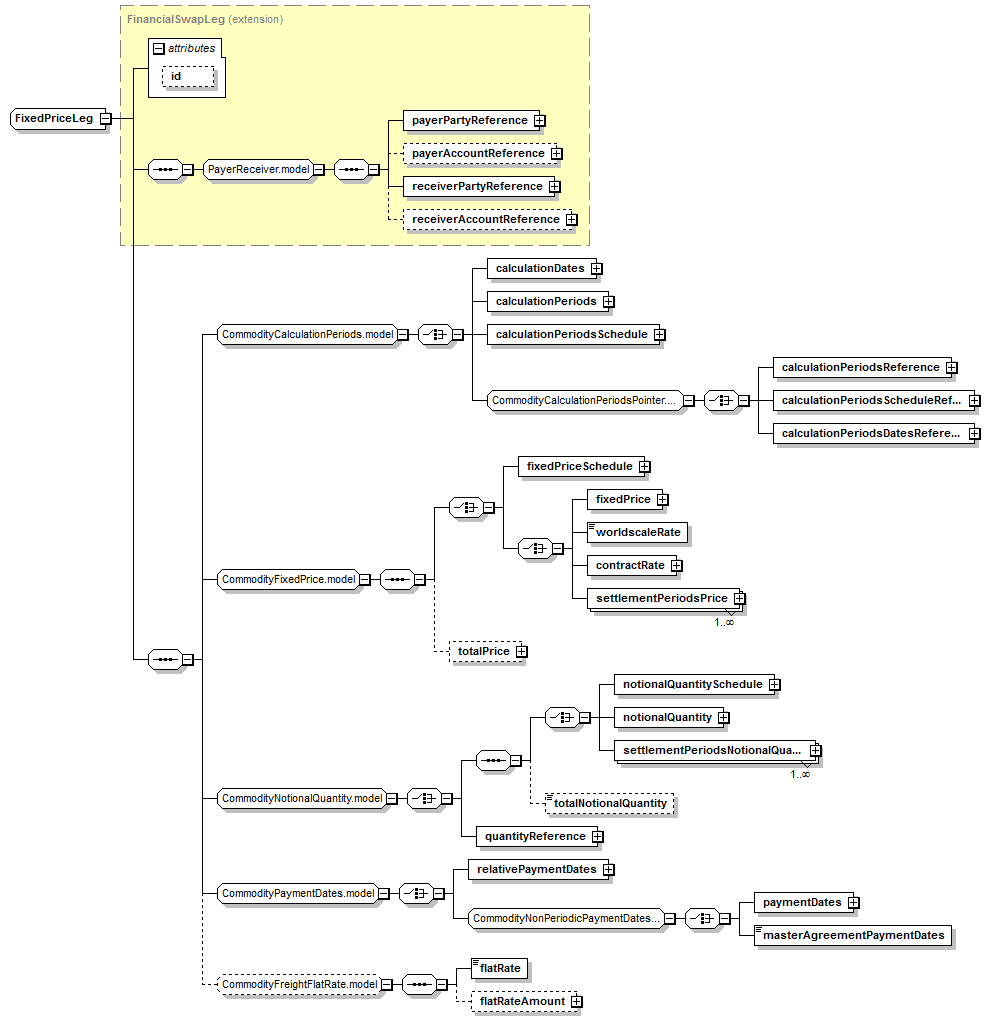

FixedPriceLeg-Fixed Price Leg of a Commodity Swap. It defines schedule of fixed payments associated with a commodity swap.

|

|

|

As with other FpML leg structures the payer and receiver parties are explicitly indicated in the 'payerPartyReference' and 'receiverPartyReference'.

The role of the remaining elements is as follows:

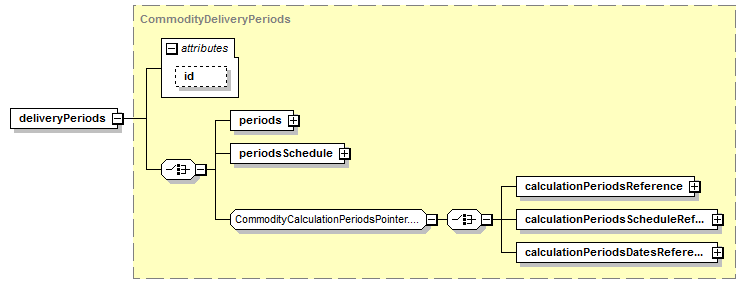

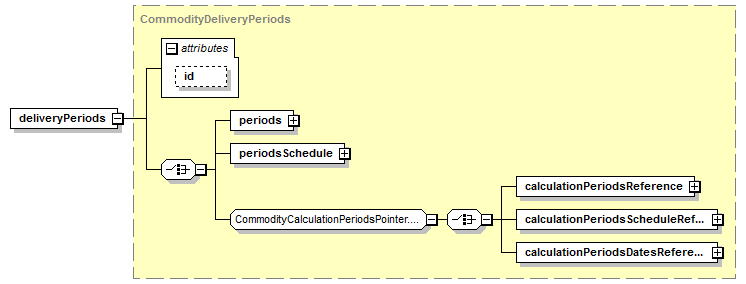

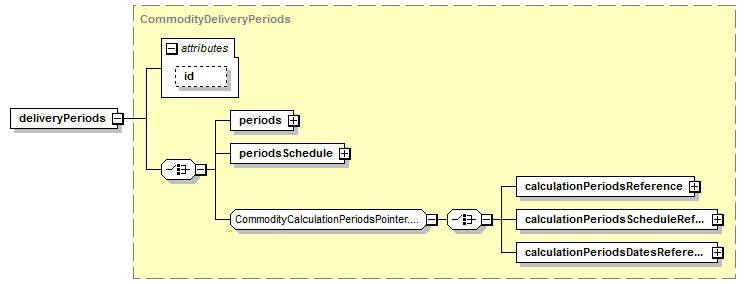

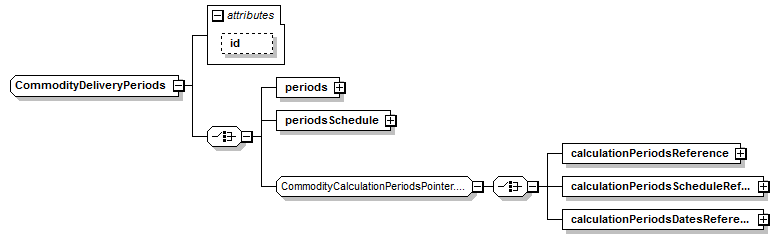

- The 'calculationPeriods' or 'calculationDates' if the Calculation Periods are all one day long or the 'calculationPeriodsSchedule' is only intended to be used if the Calculation Periods differ on each leg. If Calculation Periods mirror another leg, then the 'calculationPeriodsReference' element should be used to point to the Calculation Periods on that leg or 'calculationPeriodsDatesReference' element should be used to point to the single-day-duration Calculation Periods on that leg or the 'calculationPeriodsScheduleReference' can be used to point to the Calculation Periods Schedule for that leg.

- The 'fixedPrice' structure defines the price for a given unit of the underlying commodity where that price is fixed for the life of the trade.

- On the other hand, if the fixed price varies over the life of the trade, then the 'fixedPriceSchedule' structure is used instead of the 'fixedPrice'. Note that the intention is that a fixed price step should be specified for each Calculation Period in the trade, regardless of whether there is a change in value between two periods. This is so as to match the fixed price schedule to the calculation periods as clearly as possible. The fixed price steps must be in chronological order (i.e the first step corresponds to the first Calculation Period, the last step to the last Calculation Period).

- The 'totalPrice' structure specifies the total amount of all fixed payments due during the term of the trade.

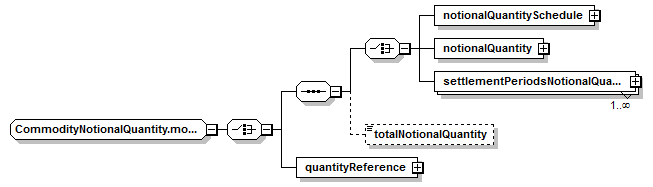

- The notional amount is specified stating either the 'notionalQuantity' or if the notional changes over the life of the transaction, then the 'notionalQuantitySchedule' is specified. The 'settlementPeriodsNotionalQuantity' should be specified for an electricity transaction, the Notional Quantity for a one or more groups of Settlement Periods to which the Notional Quantity is based. If the schedule differs for different groups of Settlement Periods, this element should be repeated. In addition, the 'totalNotionalQuantity' must be specified. Note that the intention is that a notional step should be specified for each Calculation Period in the trade, regardless of whether there is a change in value between two periods. This is so as to match the notional quantity schedule to the calculation periods as clearly as possible. The notional steps must be in chronological order (i.e the first step corresponds to the first Calculation Period, the last step to the last Calculation Period). If notional amount mirror another leg, then the 'quantityReference' element should be used to point to the Notional Quantity.

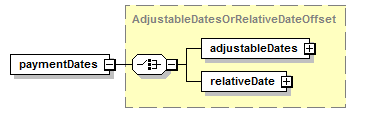

- The 'paymentDates' structure supports either the definition of dates as either a series of unadjusted dates along with a date roll convention and business calendar location list for adjustment, or as set of adjusted dates relative to some other date schedule defined elsewhere in the product (e.g. in the floating leg).

- The 'relativePaymentDates' are specified when the payment dates are relative to the calculation periods.

- The Flat Rate, applicable to Wet Voyager Charter Freight Swaps. Whether the Flat Rate is the New Worldwide Tanker Nominal Freight Scale for the Freight Index Route taken at the Trade Date of the transaction or taken on each Pricing Date. The 'flatRateAmount', If 'flatRate' is set to 'Fixed', is the actual value of the Flat Rate.

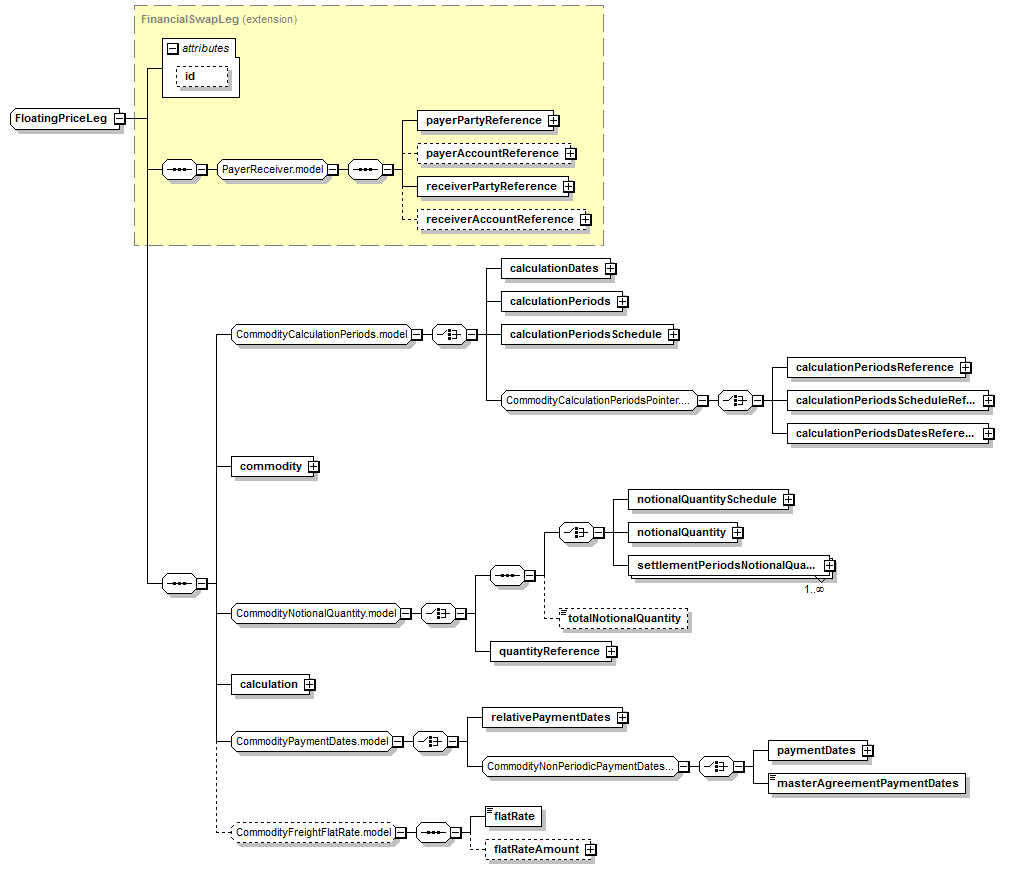

FloatingPriceLeg-Floating Price Leg of a Commodity Swap. Each 'floatingLeg' defines a series of financial payments for a commodity the value of which is derived from a floating price such as an exchange or an index publication.

|

|

|

As with the 'fixedLeg' they parties obligation to pay and receive the payments are explicitly indicated by the 'payerPartyReference' and 'receiverPartyReference' elements.

Two structures distinguish the 'floatingLeg' from the 'fixedLeg': the existence of the 'commodity' underlyer (see description above at the Commodity Underlyer section) and the 'calculation' structure within the floating leg.

16.3.4.1 calculation

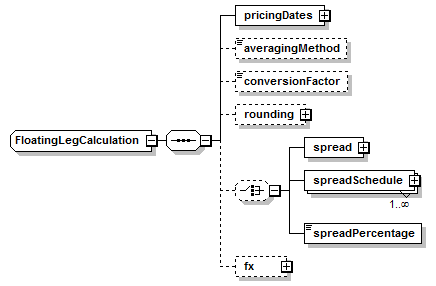

The 'calculation' structure captures details relevant to the calculation of the floating price.

FloatingLegCalculation-A type to capture details relevant to the calculation of the floating price.

The structure is defined by the following elements:

|

|

|

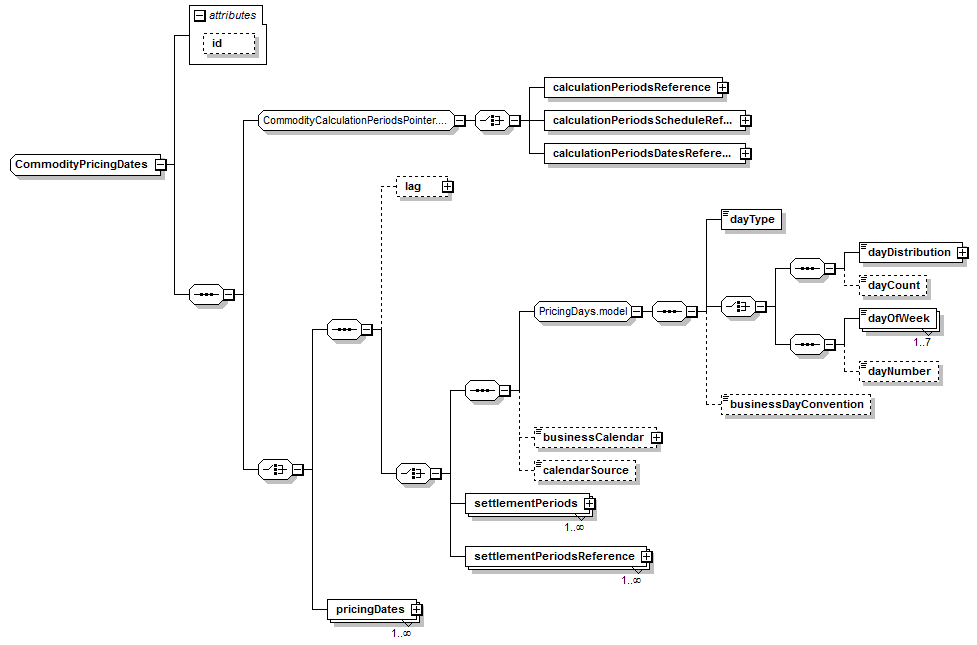

16.3.4.1.1 pricingDates

CommodityPricingDates-The dates on which prices are observed for the underlyer.

|

|

|

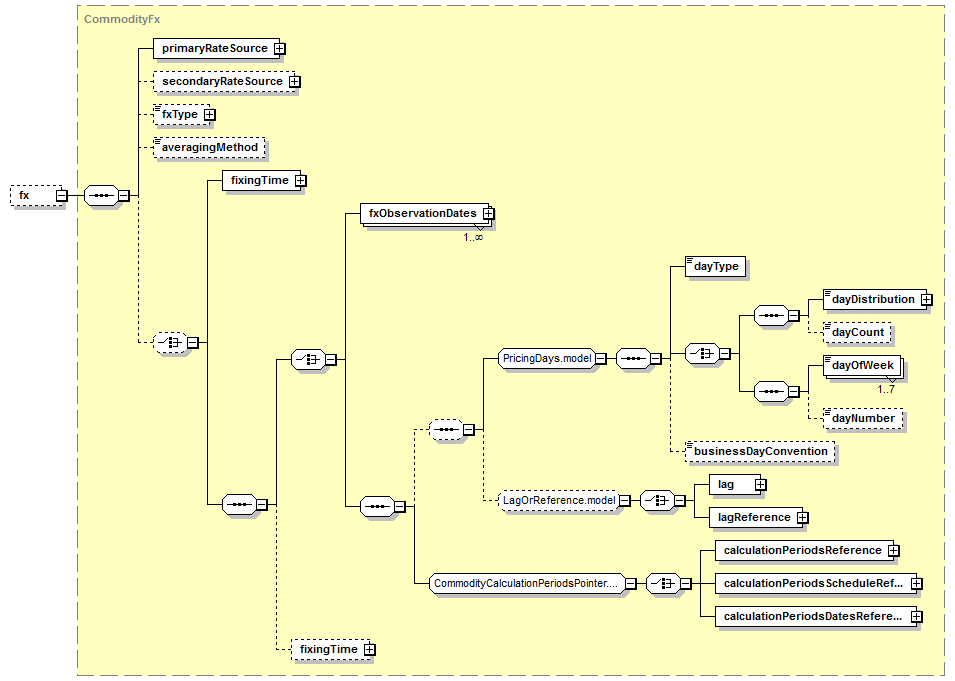

16.3.4.1.2 fx

fx-Defines how observations of FX prices are to be used to calculate a factor with which to convert the observed Commodity Reference Price to the Settlement Currency.

|

|

|

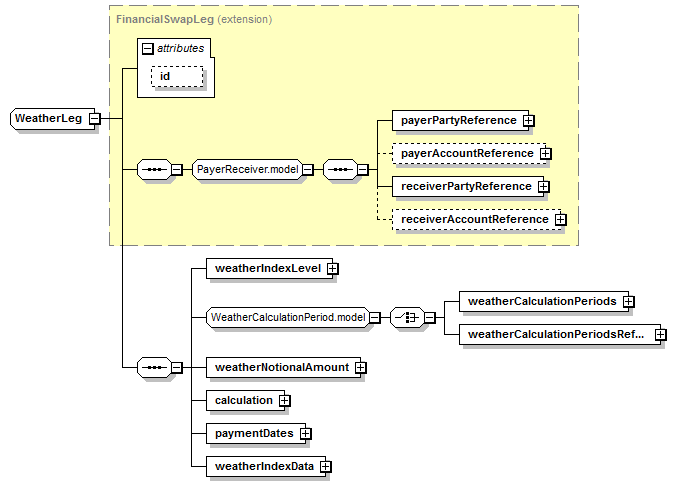

WeatherLeg-A weather leg of a Commodity Swap defines Weather Index Swap transactions. Weather Index Swap transactions are OTC derivative transactions which settle financially based on an index calculated from observations of temperature, precipitation and other weather-related measurements at weather stations throughout the world. Sub-Annex C of the 2005 ISDA Commodity Definitions provides definitions and terms for a number of types of weather indices. These indices include: HDD (heating degree days), CDD (cooling degree days), CPD (critical precipitation days). Weather Index Swap transactions result in a cash flow to one of the two counterparties each Calculation Period depending on the relationship between the Settlement Level and the Weather Index Level. A Weather Index swap transaction always consists of a commodity swap element as a parent to two weatherLeg elements.

Weather Index transaction = weatherLeg/weatherLeg.

|

|

|

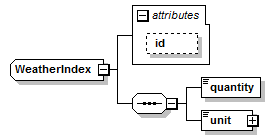

16.3.5.1 weatherLeg - WeatherIndex

WeatherIndex-A type defining the Weather Index Level or Weather Index Strike Level.

|

|

|

16.3.5.2 weatherLeg - WeatherCalculationPeriod

|

|

|

16.3.5.3 weatherLeg - weatherNotionalAmount

weatherNotionalAmount-Defines the price per weather index unit.Defines the price per weather index unit.

|

|

|

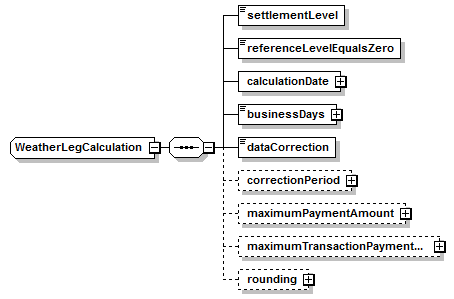

16.3.5.4 weatherLeg - calculation

WeatherLegCalculation-A type to capture details of the calculation of the Payment Amount on a Weather Index Transaction.

|

|

|

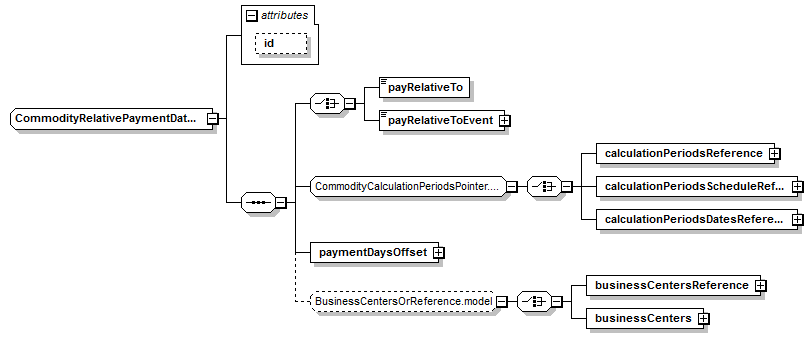

16.3.5.5 weatherLeg - paymentDates

CommodityRelativePaymentDates-The Payment Dates of the trade relative to the Calculation Periods.

|

|

|

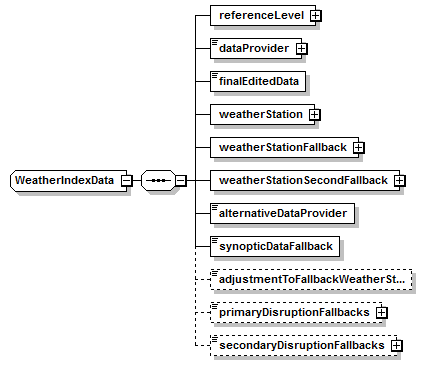

16.3.5.6 weatherLeg - weatherIndexData

WeatherIndexData-No Annotation Available

|

|

|

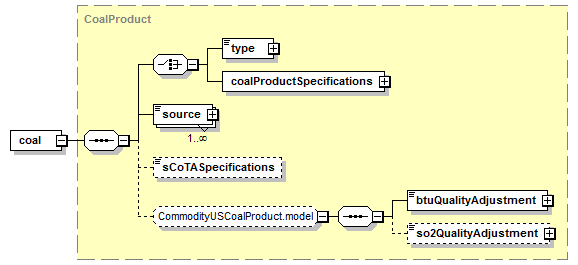

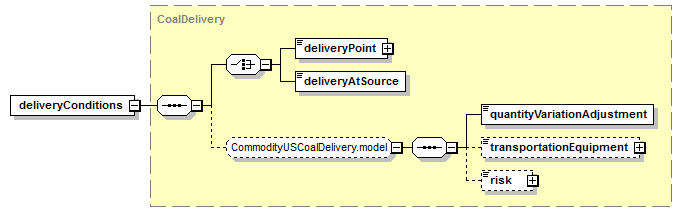

16.3.6.1 Coverage

The support for physically-settled commodity swap trades includes,

- Natural Gas

- Oil

- Electricity

- Coal

- Environmental

16.3.6.2 Product Representation

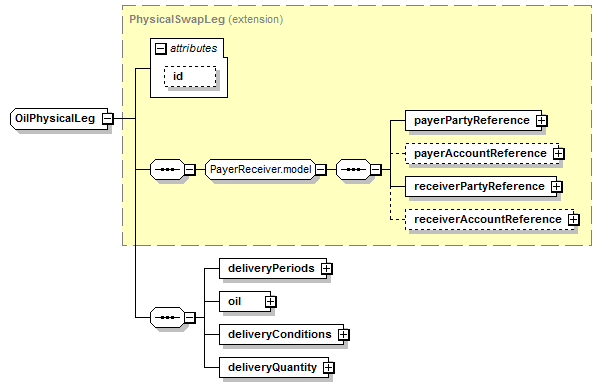

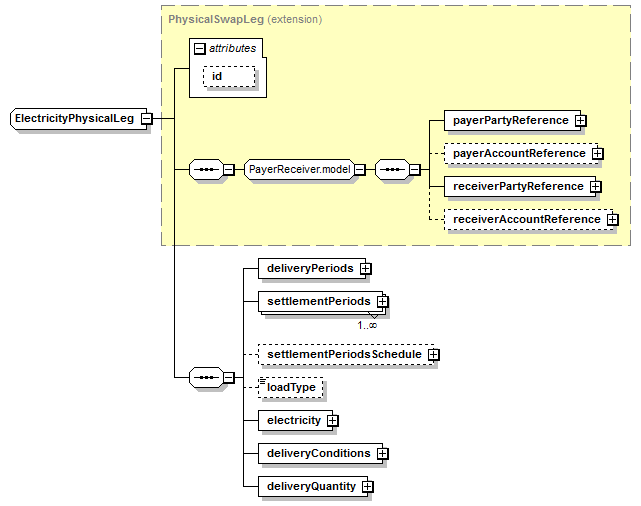

The product representation of physically-settled commodity swap or commodity forward contracts not written on a metal underlying is done within the commoditySwap product element by adding a family of physical legs.

- Fixed price transaction = xxxPhysicalLeg + fixedLeg

- Floating price transaction = xxxPhysicalLeg + floatingLeg

Note: xxx gets replaced by 'oil', 'gas', 'electricity', 'coal' or 'environmental'.

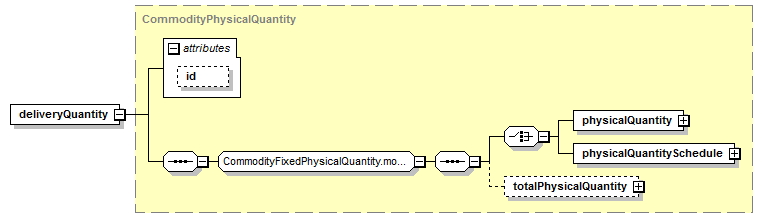

The following structures vary between all these commodities,

- Delivery periods

- Product

- Delivery

- Quantities

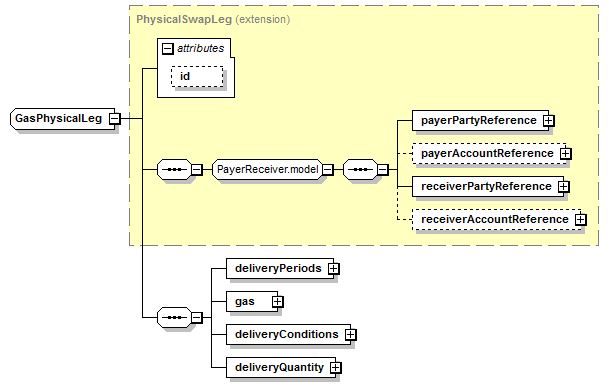

16.3.6.2.1 Gas Physical Leg

|

|

|

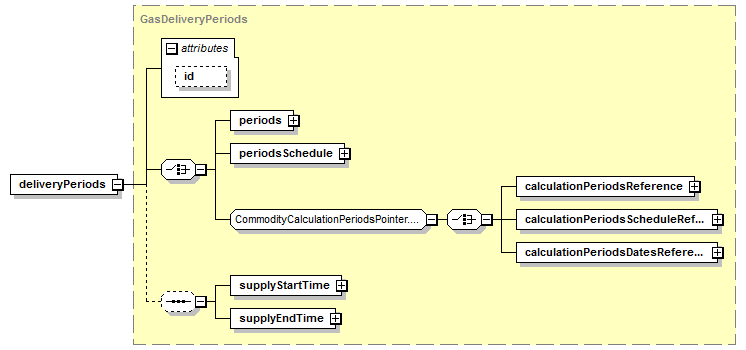

16.3.6.2.1.1 gasPhysicalLeg - deliveryPeriods

|

|

|

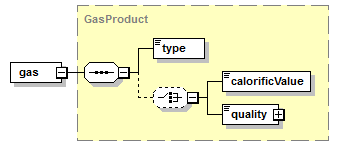

16.3.6.2.1.2 gasPhysicalLeg - product

|

|

|

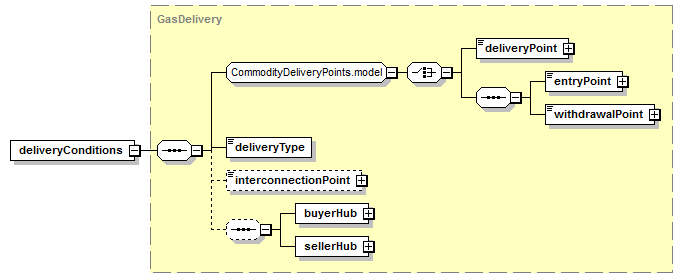

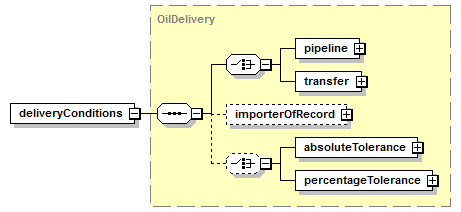

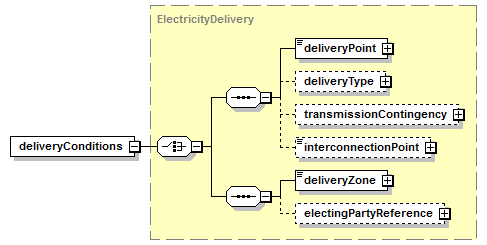

16.3.6.2.1.3 gasPhysicalLeg - deliveryConditions

|

|

|

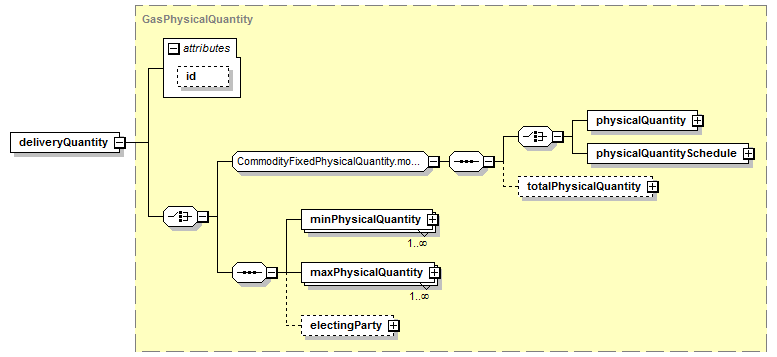

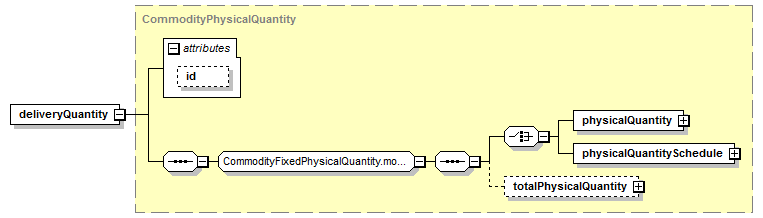

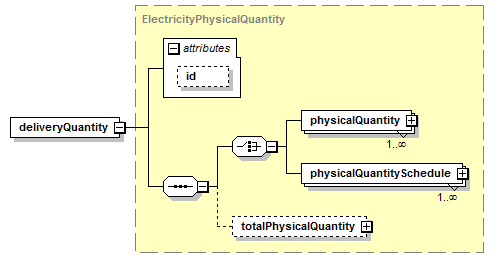

16.3.6.2.1.4 gasPhysicalLeg - deliveryQuantity

|

|

|

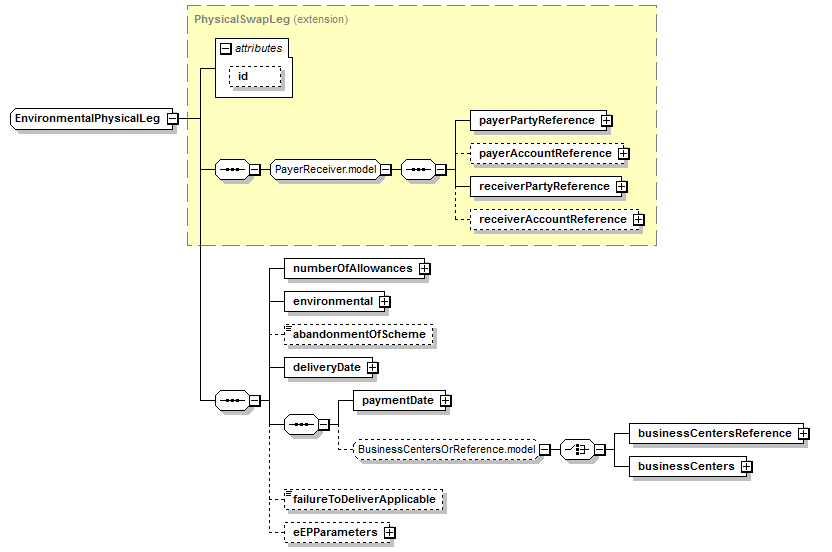

16.3.6.2.5 Environmental Physical Leg

EnvironmentalPhysicalLeg-No Annotation Available

|

|

|

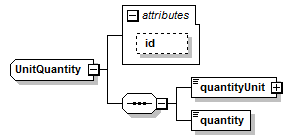

16.3.6.2.5.1 environmentalPhysicalLeg - numberOfAllowances

UnitQuantity-A quantity and associated unit.

|

|

|

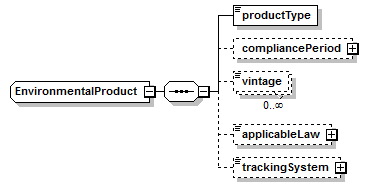

16.3.6.2.5.2 environmentalPhysicalLeg - product

EnvironmentalProduct-A type defining the characteristics of the environmental allowance or credit being traded. Settlement of environmental transactions is classified as physical because settlement is accomplished through the exchange of one or more certificates (despite the fact that this exchange is almost always executed through electronic book entry transfer between the parties allowance accounts).

|

|

|

16.3.6.2.5.3 environmentalPhysicalLeg - abandonmentOfScheme

abandonmentOfScheme-Applies to U.S. Emissions Allowance Transactions. Specifies terms which apply in the event of an Abandonment of Scheme event.Applies to U.S. Emissions Allowance Transactions. Specifies terms which apply in the event of an Abandonment of Scheme event.

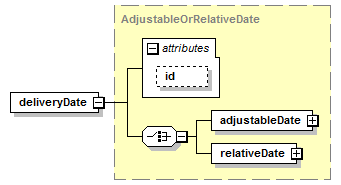

16.3.6.2.5.4 environmentalPhysicalLeg - deliveryDate

deliveryDate-The date on which allowances are to be delivered as specified in the related Confirmation.The date on which allowances are to be delivered as specified in the related Confirmation.

|

|

|

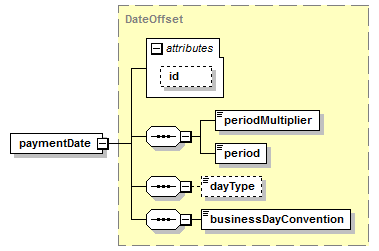

16.3.6.2.5.5 environmentalPhysicalLeg - paymentDate and businessCenters

paymentDate-No Annotation Available

|

|

|

|

|

|

16.3.6.2.5.6 environmentalPhysicalLeg - failureToDeliverApplicable

failureToDeliverApplicable-Applies to EU Emissions Allowance Transactions. Holds the Failure to Deliver (Alternative Method) election. Used to determine how provisions in Part [7] Page 7 (B) Failure to Deliver Not Remedied are to be applied.Applies to EU Emissions Allowance Transactions. Holds the Failure to Deliver (Alternative Method) election. Used to determine how provisions in Part [7] Page 7 (B) Failure to Deliver Not Remedied are to be applied.

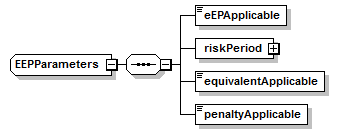

16.3.6.2.5.7 environmentalPhysicalLeg - EEPParameters

EEPParameters-Excess Emission Penalty related parameters.

|

|

|

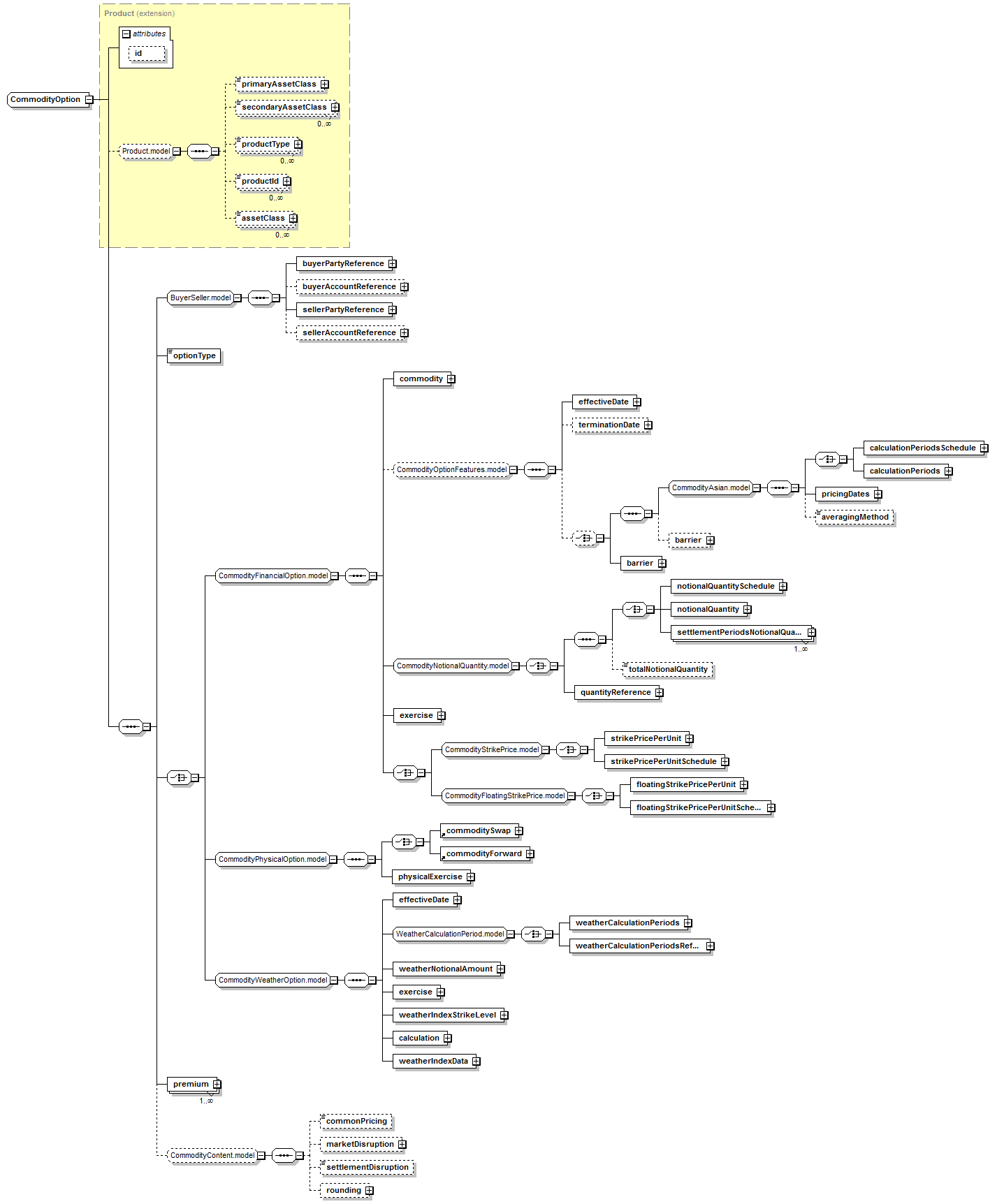

commodityOption-Defines a commodity option product. The product support for financially-settled exercises or exercise into physical forward contracts written on precious and non-precious metals. options in FpML is based on the creation of a 'commodityOption' product. The product references the 'commodity' underlyer in order to support the underlying asset of the option.

The product support for financially-settled or physically-settled forward (for preciouse and non-preciouse metal) options in FpML is based on the creation of a 'commodityOption' product. The product references the 'commodity' underlyer in order to support the underlying asset of the option.

All FpML products inherit two optional elements from the Product type: 'productType' and 'productId'. The 'productType' defines a classification of the type of product. FpML defines a simple product categorization using a coding scheme. The 'productId' contains a product reference identifier allocated by a party. In this case, FpML does not define the domain values associated with this element.

|

|

|

The choice between 'CommodityFinancialOption.model', 'CommodityPhysicalOption.model' and 'CommodityWeatherOption.model' models allows to select the financially-settled commodity options, or physically-settled forward (precious and non-precious metal) options, or weather specific option and described below.

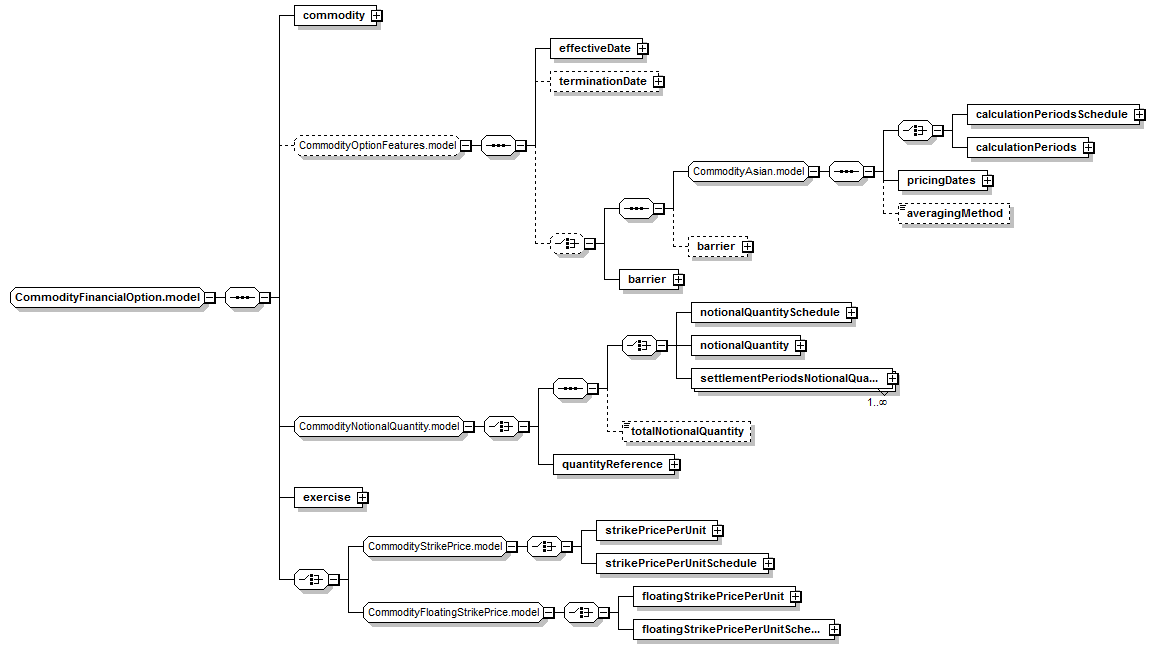

CommodityFinancialOption.model-Items specific to financially-settled commodity options.

|

|

|

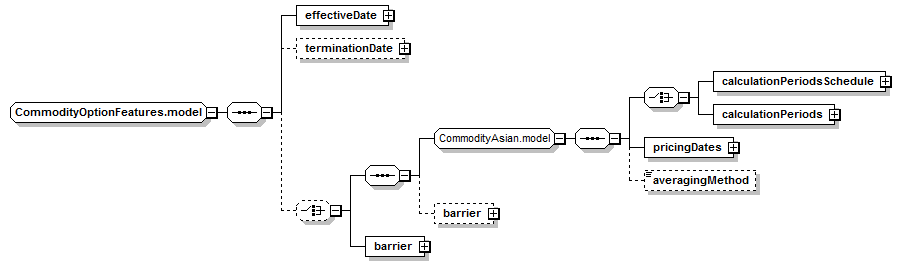

16.4.1.1 commodityOption - CommodityFinancialOption - CommodityOptionFeatures

CommodityOptionFeatures.model-Describes additional features within the option.

|

|

|

The commodity option featuers can include asian/averagin and or barrier:

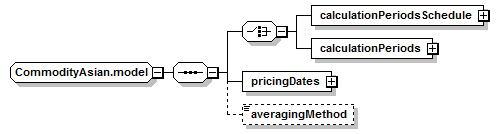

16.4.1.1.1 commodityOption - CommodityFinancialOption - CommodityOptionFeatures - CommodityAsian

CommodityAsian.model-Model group containing features specific to Asian/averaging commodity options.

The following elements are specific to asian/averaging commodity options:

|

|

|

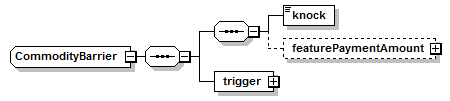

16.4.1.1.2 commodityOption - CommodityFinancialOption - CommodityOptionFeatures - CommodityBarrier

CommodityBarrier-The specification of how a barrier option will trigger (that is, knock-in or knock-out) or expire based on the position of the spot rate relative to trigger level.

The following elements are specific to commodity barrier option:

|

|

|

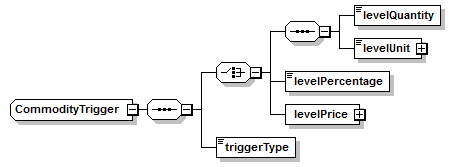

16.4.1.1.2.1 commodityOption - CommodityFinancialOption - CommodityOptionFeatures - CommodityBarrier - trigger

CommodityTrigger-The barrier which, when breached, triggers the knock-in or knock-out of the barrier option.

|

|

|

16.4.1.1.2.2 commodityOption - - CommodityFinancialOption - CommodityOptionFeatures - CommodityBarrier - Feature Payment Amount

Optional feature payment to the option buyer on knock-out.

|

|

|

16.4.1.2 commodityOption - CommodityFinancialOption - CommodityNotionalQuantity

As with the 'commoditySwap', the notional amount of the 'commodityOption' is specified stating either the 'notionalQuantity' or if the notional changes over the life of the transaction, then the 'notionalQuantitySchedule' is specified. In addition, the 'totalNotionalQuantity' must be specified. Note that the intention is that a notional step should be specified for each Calculation Period in the trade, regardless of whether there is a change in value between two periods. This is so as to match the notional quantity schedule to the calculation periods as clearly as possible. The notional steps must be in chronological order (i.e the first step corresponds to the first Calculation Period, the last step to the last Calculation Period).

|

|

|

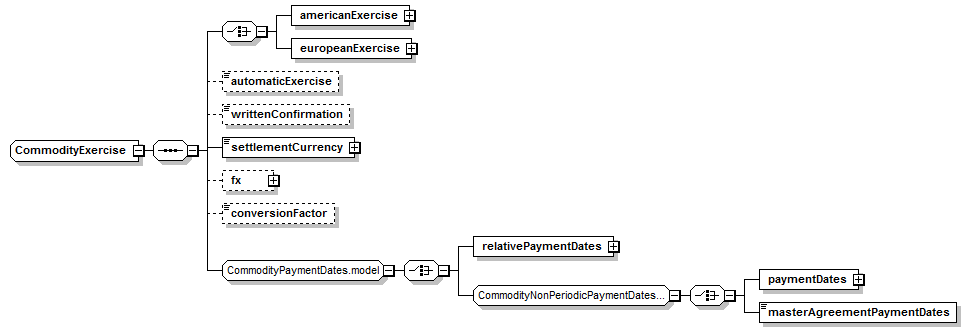

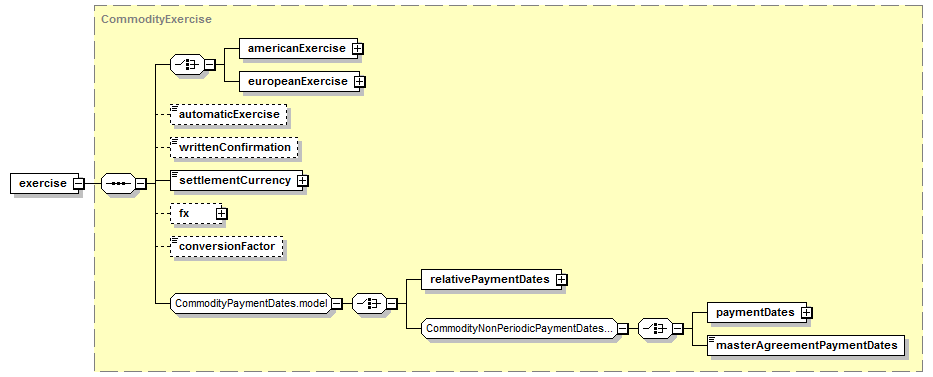

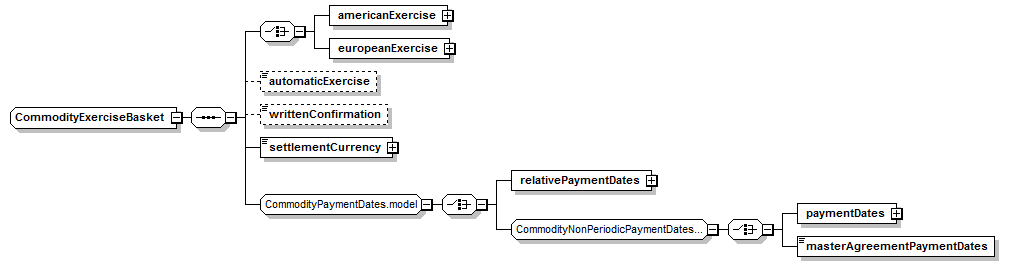

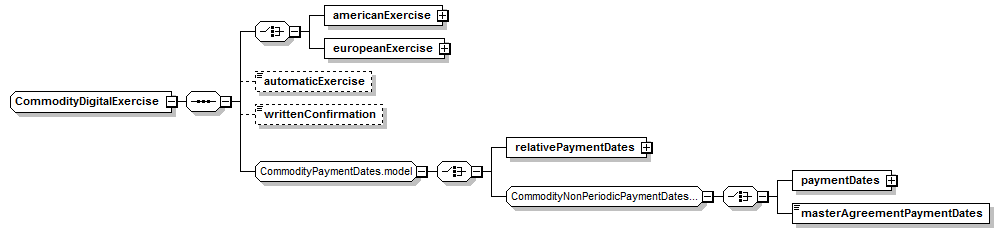

16.4.1.3 commodityOption - CommodityFinancialOption - CommodityExercise

CommodityExercise-The parameters for defining how the commodity option can be exercised, how it is priced and how it is settled.

|

|

|

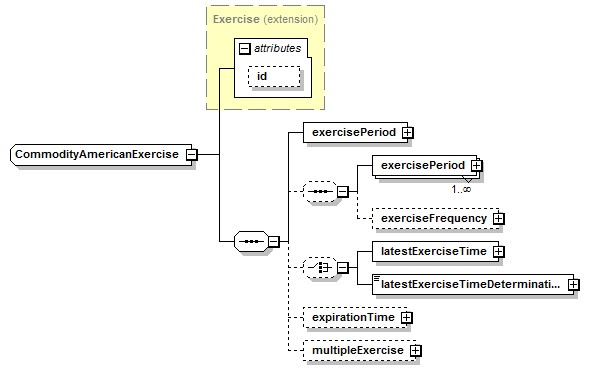

16.4.1.3.1 CommodityAmericanExercise

CommodityAmericanExercise-A type for defining exercise procedures associated with an American style exercise of a commodity option.

|

|

|

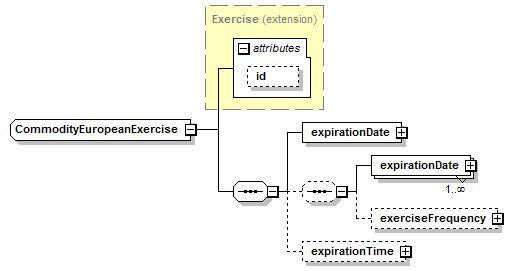

16.4.1.3.2 CommodityEuropeanExercise

CommodityEuropeanExercise-A type for defining exercise procedures associated with a European style exercise of a commodity option.

|

|

|

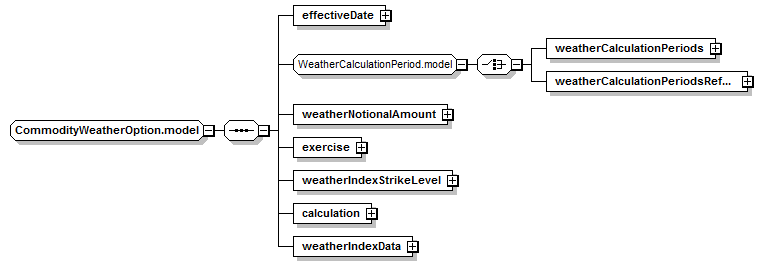

CommodityWeatherOption.model-Described Weather Index Option component. Weather Index Option transactions are OTC derivative transactions which settle financially based on an index calculated from observations of temperature and precipitation at weather stations throughout the world. Sub-Annex C of the 2005 ISDA Commodity Definitions provides definitions and terms for a number of types of weather indices. These indices include: HDD (heating degree days), CDD (cooling degree days), CPD (critical precipitation days). Weather Index Option Transactions results in a cash flow to the buyer depending on the relationship between the Settlement Level to the Weather Index Strike Level.

|

|

|

effectiveDate is an effectiveDate of a Weather Index Option.

16.4.2.1 commodityOption - CommodityWeatherOption - WeatherCalculationPeriod

WeatherCalculationPeriod.model-Descriptions of a calculation period.

Weather Index Swap and Weather Index Option transactions are OTC derivative transactions which settle financially based on a index calculated from observations of temperature and precipitation at weather stations throughout the world. Sub-Annex C of the 2005 ISDA Commodity Definitions provides definitions and terms for a number of types of weather indices. These indices include: HDD (heating degree days), CDD (cooling degree days), CPD (critical precipitation days). Weather Index Swap transactions result in a cash flow to one of the two counterparties each Calculation Period depending on the relationship between the Settlement Level and the Weather Index Level. Weather Index Option Transactions results in a cash flow to to the buyer if depending on the relationship between the Settlement Level to the Weather Index Strike Level.

|

|

|

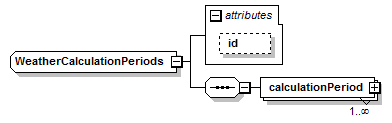

16.4.2.1.1 WeatherCalculationPeriods

WeatherCalculationPeriods-The schedule of Calculation Period First Days and Lasts Days. If there is only one First Day - Last Day pair then the First is equal to the Effective Date and the Last Day is equal to the Termination Date.

|

|

|

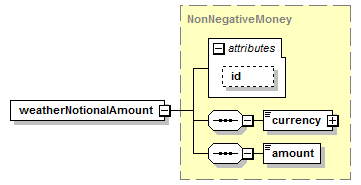

16.4.2.2 commodityOption - CommodityWeatherOption - weatherNotionalAmount

weatherNotionalAmount-No Annotation Available

|

|

|

16.4.2.3 commodityOption - CommodityWeatherOption - exercise

exercise-No Annotation Available

|

|

|

16.4.2.4 commodityOption - CommodityWeatherOption - weatherIndexStrikeLevel

weatherIndexStrikeLevel-Weather Index strike price level is specified in terms of weather index units (e.g. 1 Days, 3 Inches, etc.)

|

|

|

16.4.2.5 commodityOption - CommodityWeatherOption - calculation

calculation-Contains parameters which figure in the calculation of payments on a Weather Index Option.

|

|

|

16.4.2.6 commodityOption - CommodityWeatherOption - weatherIndexData

weatherIndexData-Specifies where the data (e.g. CPD) have been collected, an actual physical reference point (weather station) and various fall back arrangements.

|

|

|

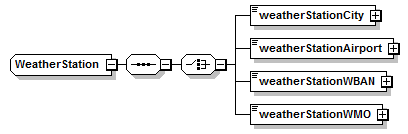

16.4.2.6.1 WeatherStation

WeatherStation-Weather Station.

The same content applies to 'weatherStationFallback' and 'weatherStationSecondFallback'.

|

|

|

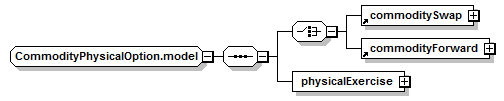

CommodityPhysicalOption.model-Items specific to financially-settled commodity options.

The approach is similar to that used for interest rate swaptions by embedding a physically-settled precious and non-precious metal forward transaction within the option transaction. So that the exercise of an option results in a new physically-settled forward transaction.

|

|

|

The 'commodityForward' component is described in the 'Commodity Forward' section below.

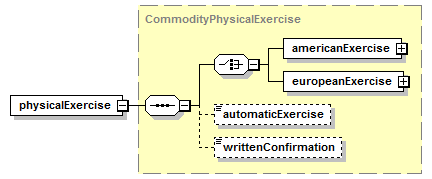

The 'physicalExercise' component is the same as for physically-settled commodity options described in the 'commoditySwaption' section below.

NOTE: support for other physically-settled options within 'commodityOption' is DEPRICATED. The 'commoditySwaption' product should be used instead.

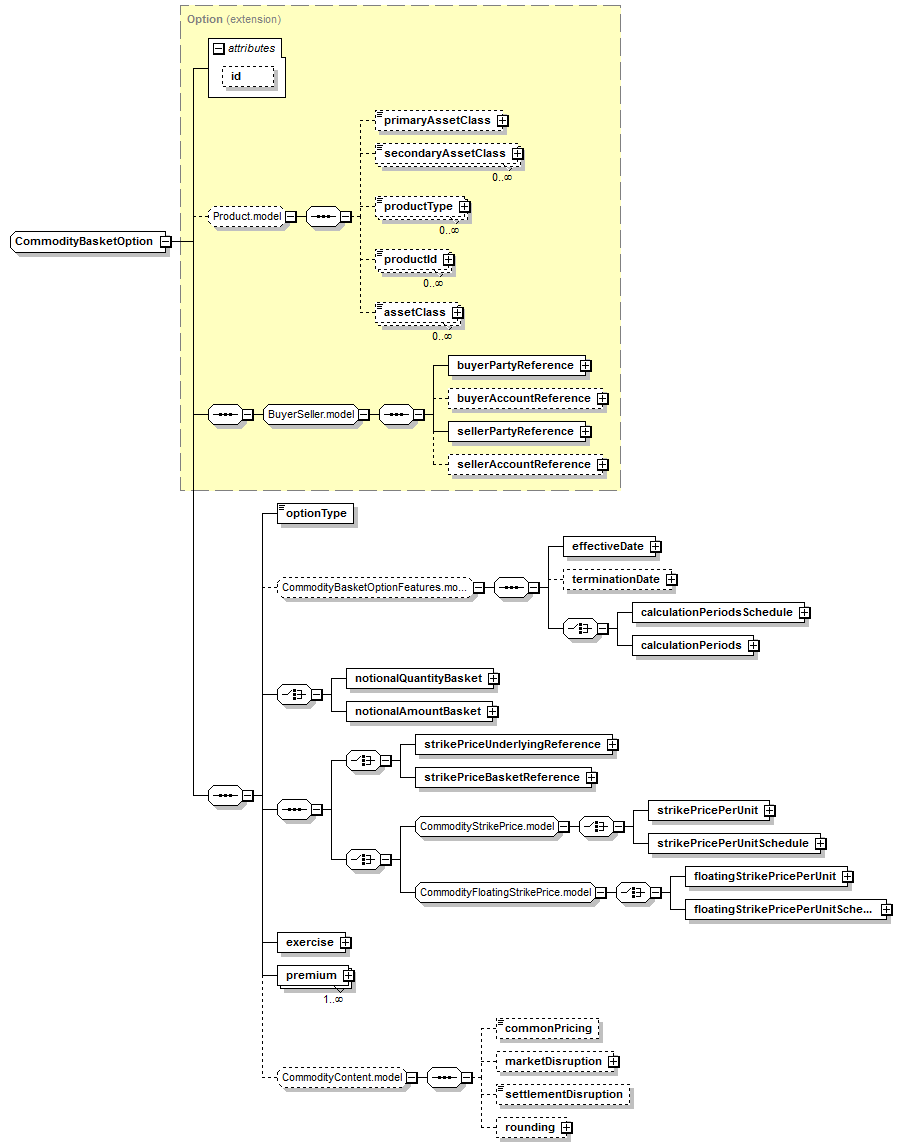

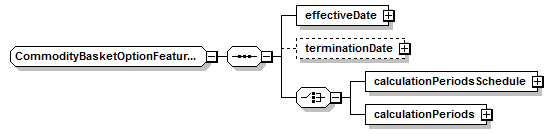

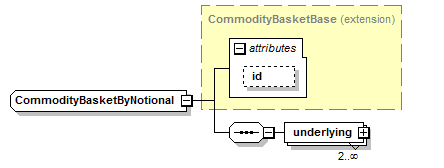

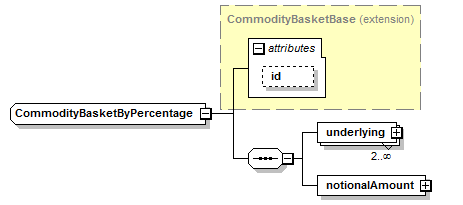

The commodityBasketOption defines a commodity basket option product

|

|

|

Describes additional features within the Basket option

|

|

|

Describes notional quantity basket.

|

|

|

Describes notional amount basket.

|

|

|

Describes strike price.

|

|

|

Describes floating strike price.

|

|

|

|

|

|

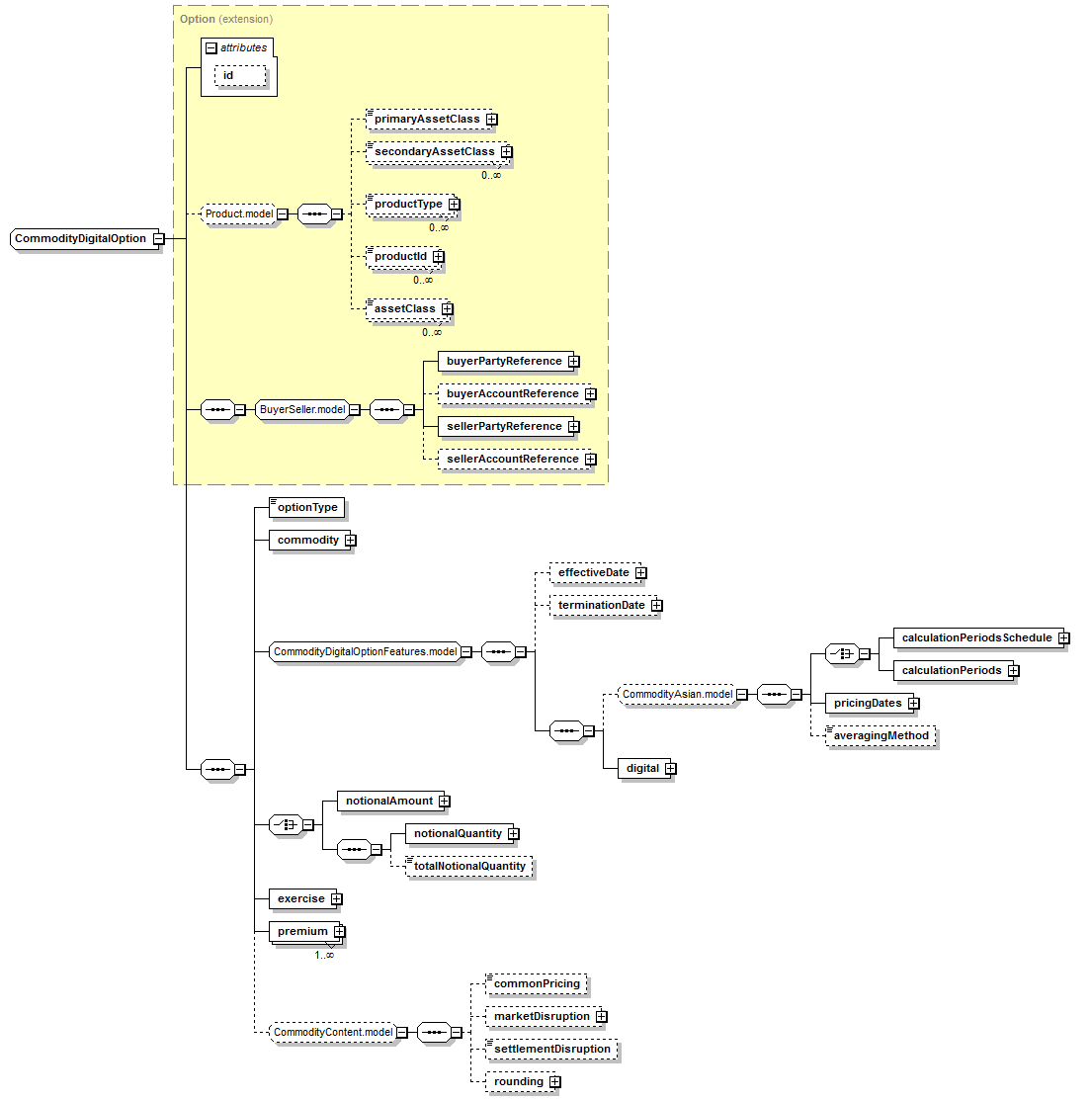

The commodityDigitalOption defines a commodity digital option product

|

|

|

Specific to financially-settled commodity digital options

|

|

|

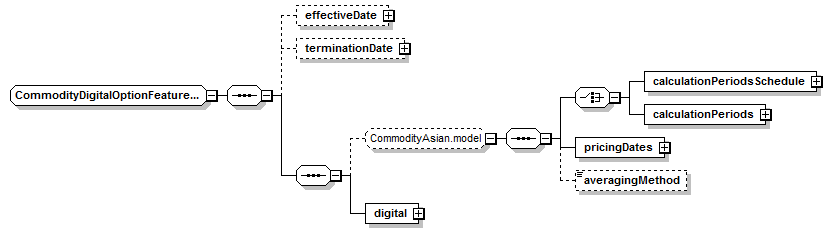

16.6.1.1 commodityDigitalOption - CommodityDigitalOptionFeatures.model - digital

Specific the commodity digital options' barrier:

|

|

|

16.6.1.1.1 commodityDigitalOption - CommodityDigitalOptionFeatures.model - Digital - Commodity Trigger

Trigger point at which feature is effective.

|

|

|

|

|

|

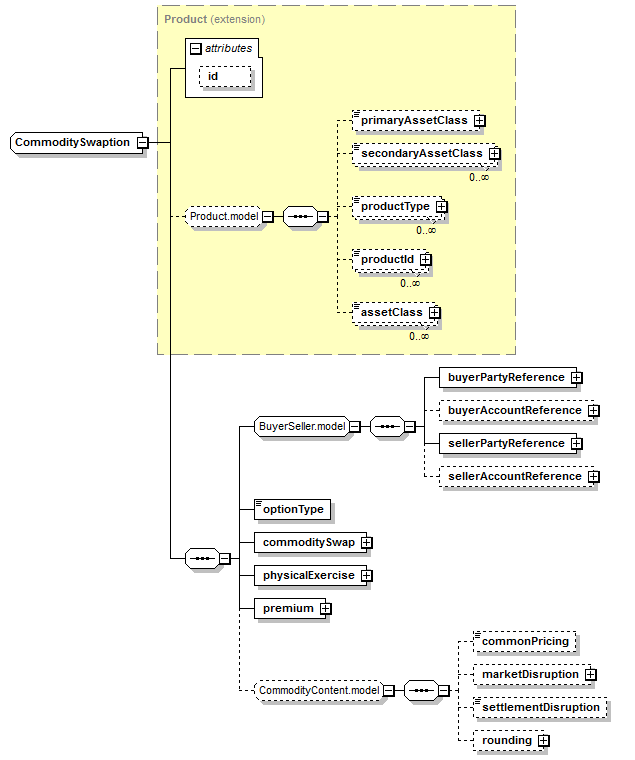

The commoditySwaption is specific to physically-settled commodity options:

All FpML products inherit two optional elements from the Product type: 'productType' and 'productId'. The 'productType' defines a classification of the type of product. FpML defines a simple product categorization using a coding scheme. The 'productId' contains a product reference identifier allocated by a party. In this case, FpML does not define the domain values associated with this element.

|

|

|

The approach is similar to that used for interest rate swaptions by embedding a physically-settled swap transaction within the option transaction. So that the exercise of an option results in a new physically-settled swap transaction.

|

|

|

physicalExercise-The parameters for defining how the commodity option can be exercised into a physical transaction.The parameters for defining how the commodity option can be exercised into a physical transaction.

|

|

|

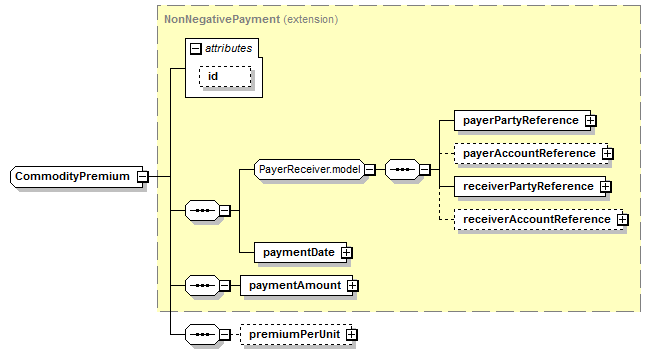

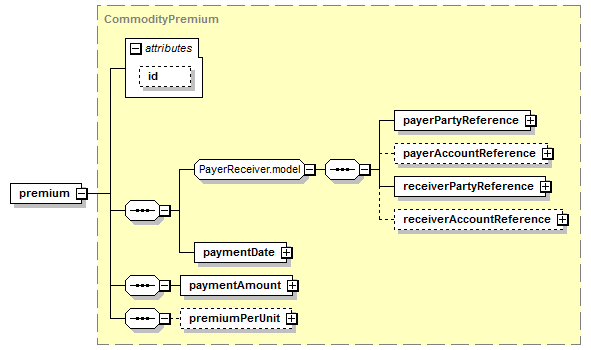

premium-The option premium payable by the buyer to the seller.The option premium payable by the buyer to the seller.

Should the premium differ over the course of an Asian options life (e.g. because delivery is per calendar day which is reflected in the premium), a premium schedule should be specified. Note that the intention is that a premium step should be specified for each Calculation Period in the trade, regardless of whether there is a change in value between two periods. This is so as to match the premium schedule to the calculation periods as clearly as possible. The premium steps must be in chronological order (i.e the first step corresponds to the first Calculation Period, the last step to the last Calculation Period).

|

|

|

CommodityContent.model-Items common to all Commodity Transactions.

The 'commonPricing', 'marketDisruption', and 'rounding' elements are common across all commodity transactions. For a detailed description of them see the commoditySwap section.

|

|

|

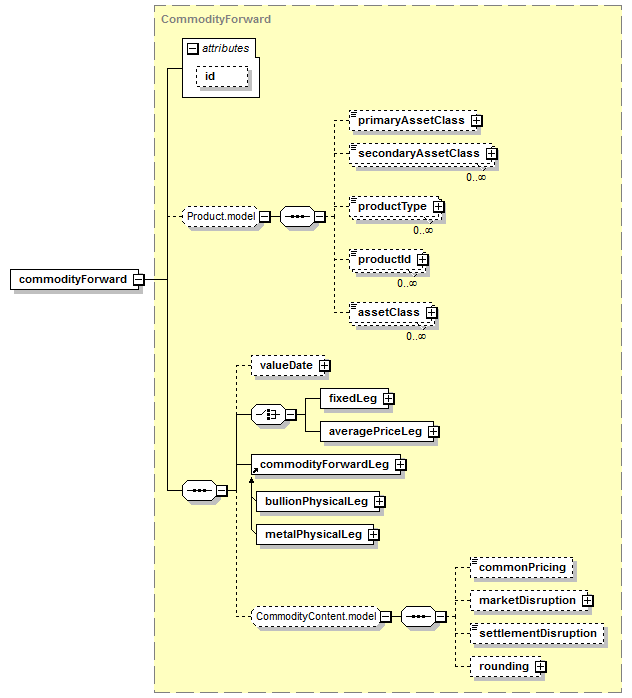

The commodityForward product element supports the representation of Precious and Non-Precious metal Forwards. Whilst some commodity forwards are booked as single period swaps, precious forwards are extremely basic trades and are confirmed under a different ISDA confirmation template

Even though the initial scope is limited to Precious and Non-Precious Forward, the intention of the working group is to allow support for other commodity classes should this be required.

|

|

|

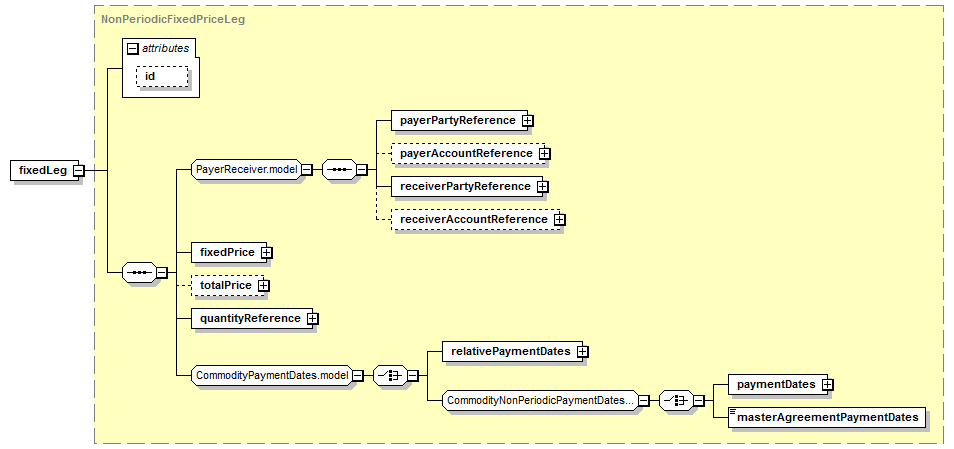

The fixed payment of the Commodity Forward product is represented using the fixedLeg element of type NonPeriodicFixedPriceLeg.

|

|

|

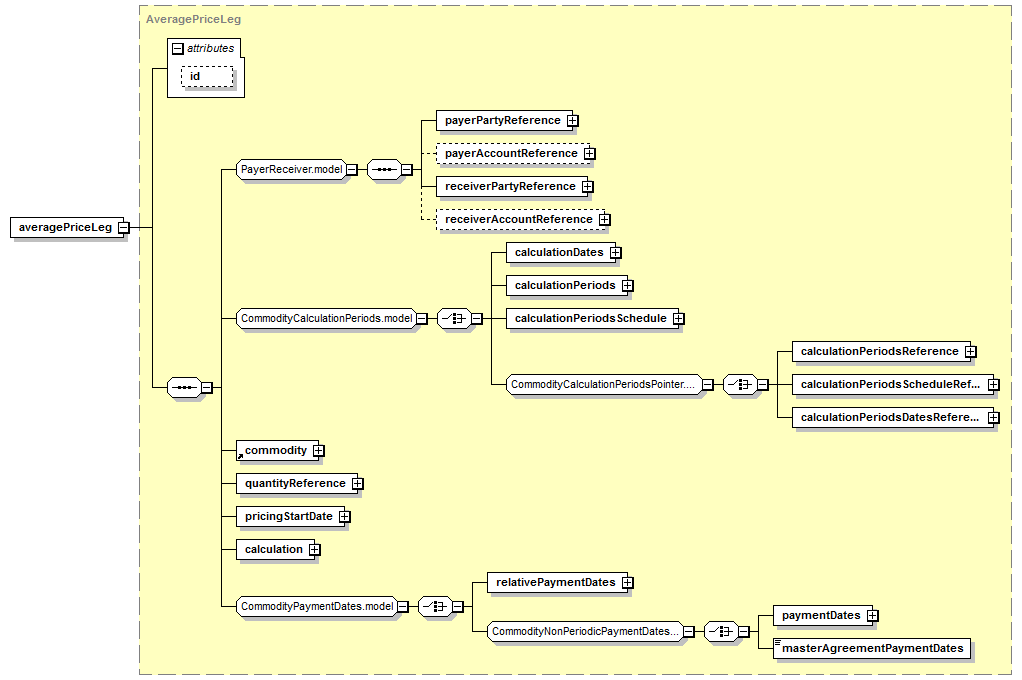

averagePriceLeg-Specifies the calculated floating price leg of a Commodity Forward Transaction.

|

|

|

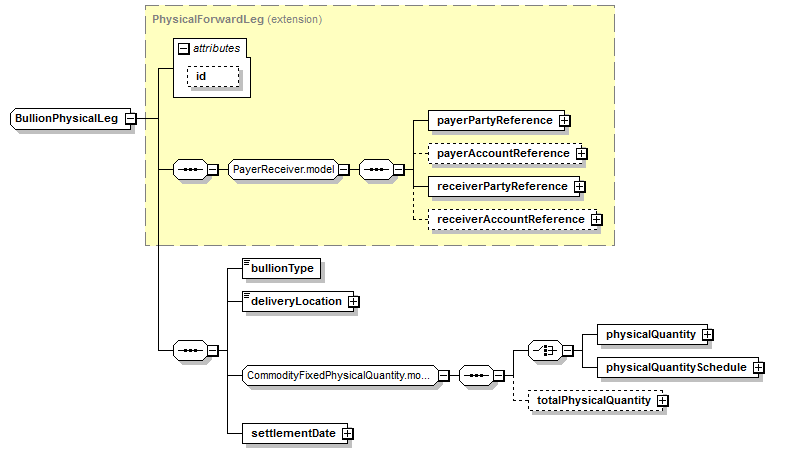

The 'commodityForwardLeg' element is placeholder within commodityForward structure for the actual Precious and Non-Precious metal legs (e.g. bullionPhysicalLeg and metalPhysicalLeg).

The intention of the new leg is to re-use as many existing commodity components as possible to achieve a flexible implementation of a forward that will be adaptable for use with further commodity classes.

Consequently, the BullionPhysicalLeg component will be a member of a choice group such that further commodity types can be added over time.

|

|

|

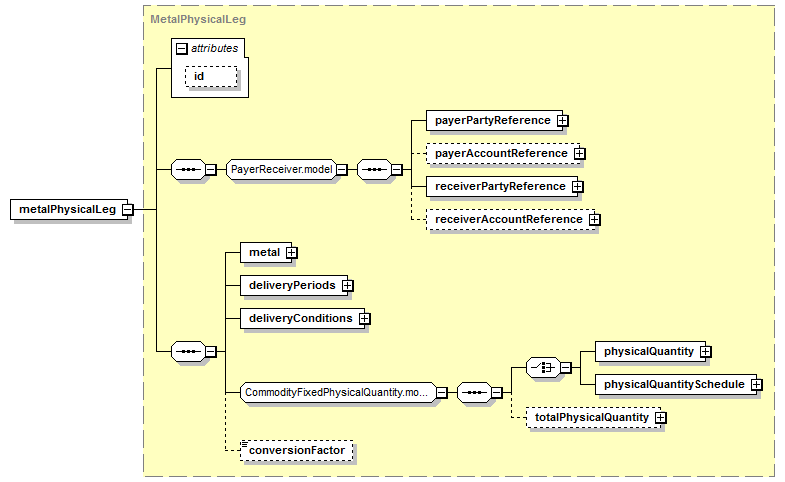

metalPhysicalLeg-Physically settled metal products leg.

|

|

|

16.8.4.1 commodityForward - metalPhysicalLeg - metal

metal-The specification of the Metal Product to be delivered.The specification of the Metal Product to be delivered.

|

|

16.8.4.2 commodityForward - metalPhysicalLeg - deliveryPeriods

deliveryPeriods-The period during which delivery/deliveries of Metal may be scheduled.The period during which delivery/deliveries of Metal may be scheduled.

|

|

|

16.8.4.3 commodityForward - metalPhysicalLeg - deliveryConditions

deliveryConditions-The physical delivery arrangements and requirements for a physically settled non-precious metal transaction.The physical delivery arrangements and requirements for a physically settled non-precious metal transaction.

|

|

|

16.8.4.4 commodityForward - metalPhysicalLeg - CommodityFixedPhysicalQuantity.model

CommodityFixedPhysicalQuantity.model-The different options for specifying a fixed physical quantity of commodity to be delivered.

|

|

|