Namespace: |

|

Content: |

complex, 1 attribute, 12 elements |

Defined: |

globally in fpml-eq-shared-5-3.xsd; see XML source |

Includes: |

definitions of 5 elements |

Used: |

at 1 location |

XML Representation Summary |

||||||

| <... | ||||||

|

||||||

| > | ||||||

| </...> | ||||||

Type Derivation Tree |

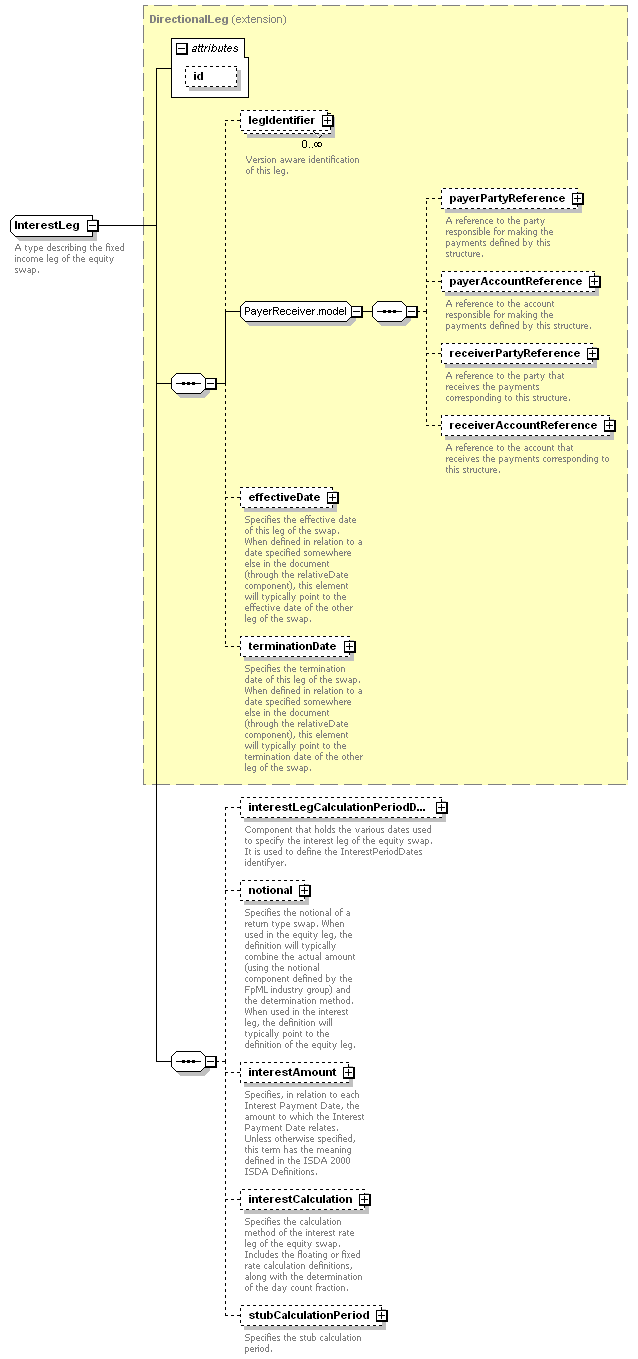

| <xsd:complexType name="InterestLeg"> <xsd:complexContent> <xsd:sequence> <xsd:element minOccurs="0" name="interestLegCalculationPeriodDates" type="InterestLegCalculationPeriodDates"/> </xsd:sequence> </xsd:extension> </xsd:complexContent> </xsd:complexType> |

Type: |

LegAmount, complex content |

| <xsd:element minOccurs="0" name="interestAmount" type="LegAmount"/> |

Type: |

InterestCalculation, complex content |

| <xsd:element minOccurs="0" name="interestCalculation" type="InterestCalculation"/> |

Type: |

InterestLegCalculationPeriodDates, complex content |

| <xsd:element minOccurs="0" name="interestLegCalculationPeriodDates" type="InterestLegCalculationPeriodDates"/> |

Type: |

ReturnSwapNotional, complex content |

| <xsd:element minOccurs="0" name="notional" type="ReturnSwapNotional"/> |

Type: |

StubCalculationPeriod, complex content |

| <xsd:element minOccurs="0" name="stubCalculationPeriod" type="StubCalculationPeriod"/> |

| XML schema documentation generated with DocFlex/XML 1.8.6b2 using DocFlex/XML XSDDoc 2.5.1 template set. All content model diagrams generated by Altova XMLSpy via DocFlex/XML XMLSpy Integration. |