Namespace: |

|

Type: |

|

Content: |

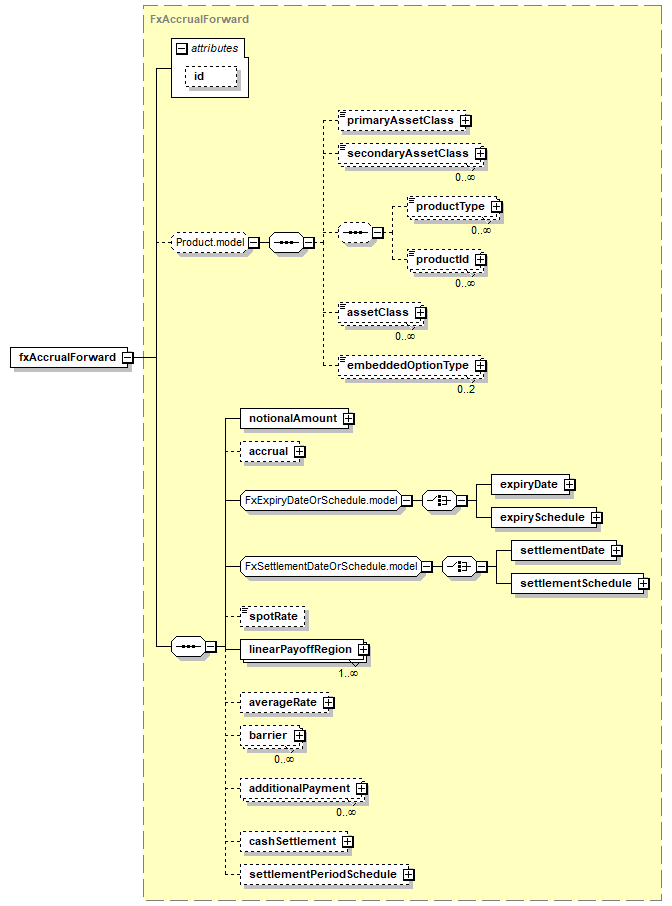

complex, 1 attribute, 19 elements |

Subst.Gr: |

may substitute for element product |

Defined: |

globally in fpml-fx-accruals-5-10.xsd; see XML source |

Used: |

never |

XML Representation Summary |

||||||

<fxAccrualForward |

||||||

|

||||||

> |

||||||

|

||||||

</fxAccrualForward> |

||||||

|

XML schema documentation generated with DocFlex/XML 1.10b5 using DocFlex/XML XSDDoc 2.8.1 template set. All content model diagrams generated by Altova XMLSpy via DocFlex/XML XMLSpy Integration.

|