Namespace: |

|

Content: |

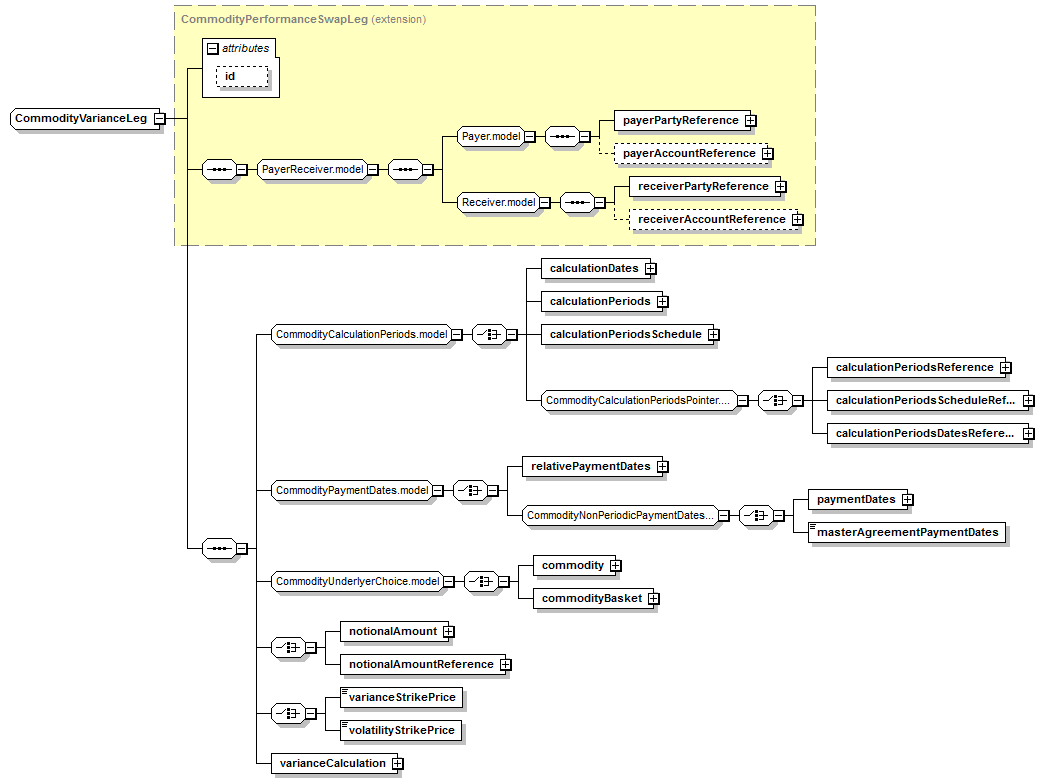

complex, 1 attribute, 20 elements |

Defined: |

globally in fpml-com-5-8.xsd; see XML source |

Includes: |

definitions of 5 elements |

Used: |

at 1 location |

XML Representation Summary |

||||||

<... |

||||||

|

||||||

> |

||||||

</...> |

||||||

|

Type Derivation Tree

|

|

<xsd:complexContent>

<xsd:extension base="CommodityPerformanceSwapLeg">

<xsd:sequence>

<xsd:group ref="CommodityCalculationPeriods.model"/>

<xsd:choice>

</xsd:choice>

<xsd:choice>

</xsd:choice>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|

Type: |

CommodityNotionalAmount, complex content |

Type: |

CommodityNotionalAmountReference, empty content |

Type: |

CommodityVarianceCalculation, complex content |

Type: |

xsd:decimal, predefined, simple content |

Type: |

xsd:decimal, predefined, simple content |

|

XML schema documentation generated with DocFlex/XML 1.9.0 using DocFlex/XML XSDDoc 2.8.0 template set. All content model diagrams generated by Altova XMLSpy via DocFlex/XML XMLSpy Integration.

|